Europe to keep importing ethylene from US، eyes Asian barrels.

Petrotahlil :

Europe to remain most expensive region.

Asia steam cracker run cut in focus.

Europe is likely to continue to import ethylene, mainly from the US and possibly from Asia, in the second-half of 2019 as supply in Europe is expected to remain limited, while the US and Asia are expected to be inundated with supplies.

In the middle of this year, an arbitrage window for ethylene to move from Asia to Europe was technically open, after the ethylene price spread between the two locations widened to around $300/mt.

“It’s a big change.

Europe is structurally long, and [the] most expensive region in the world,” one trader said.

Market sources said ethylene demand in Europe slowed down somewhat in July following the re-start of large crackers in Northwest Europe as well as the start of the summer holidays.

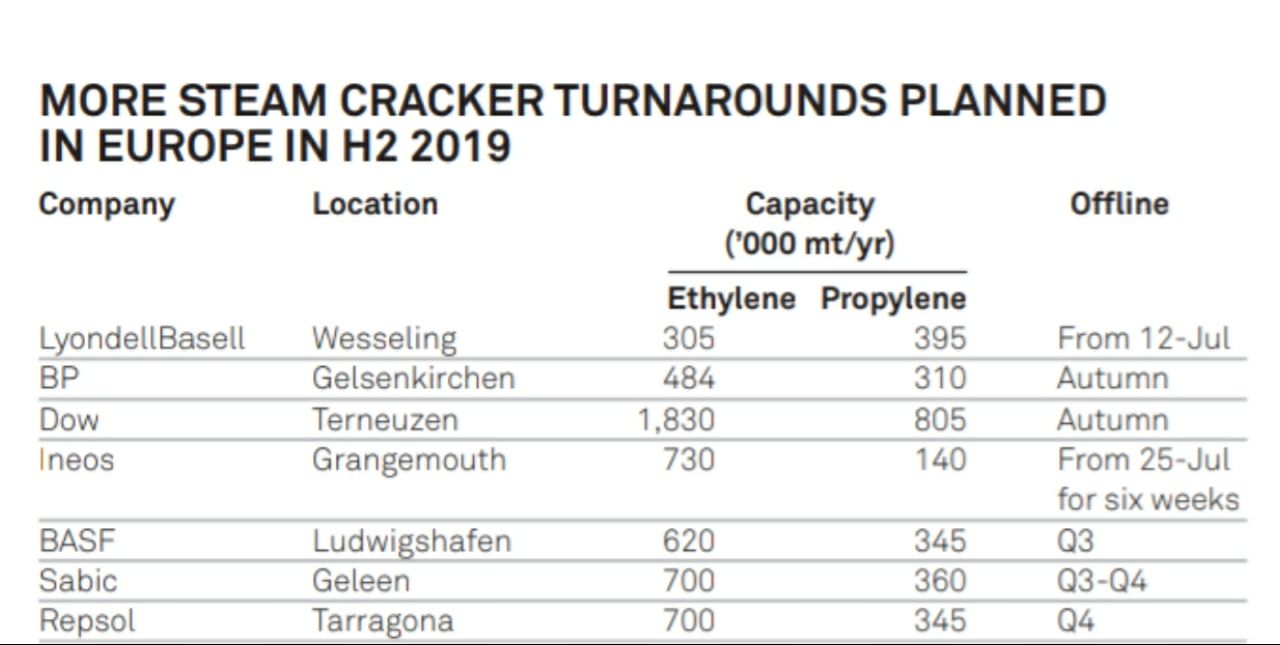

There is expectation that supply for the rest of the year will experience some degree of tightness due to scheduled maintenance at some plants, with any insufficiencies to be met by imports.

Should there be any turnaround, it is due to take place from late August to end of October.

Europe is likely to continue to import ethylene from the US, where supplies are ample. For 2019, five new startups are expected in the US Gulf, with capacity totaling just under 5 million mt/year. Thus far, only two out of these five plants have come on line in 2019: Indorama’s 440,000 mt/year cracker and Westlake-Lotte’s 1 million mt/year cracker, both in Lake Charles.

Market participants still expect Shintech’s 500,000 mt/year cracker and Sasol’s 1.5 million mt/year cracker to come on line during the summer, both of which are also located in Lake Charles. That leaves Formosa Plastics 1.5 million mt/year cracker in Point Comfort, Texas, which is expected to come on line by the end of the year, concluding this first wave of new ethylene cracker startups.

US ethylene exports is also likely to increase from later this year in line with the planned start up of a new ethylene, export terminal.

Enterprise Products Partners and its project partner Navigator Gas is on schedule to complete its new 1 million mt/year ethylene export terminal at Morgan’s Point, Texas, near the mouth of the Houston Ship Channel, by the end of 2019. Enterprise has already converted a 5.3 million-barrel ethane cavern to hold ethylene in the second quarter of this year at its operations in Mont Belvieu, the US natural gas liquids hub, east of Morgan’s Point.

Asian supply set to rise in H2

Asian ethylene supplies are also expected to increase towards the end of this year as maintenance is completed at key steam crackers. Some steam crackers are scheduled to be shut for planned turnaround in H2, such as Formosa’s No.

2 cracker and CPC’s No.4 unit. Despite these turnarounds, supplies are still expected to increase in line with the planned start up of new steam crackers such as SP Chemical and RAPID.

SP Olefins (Taixing) Co. Ltd, a unit of Singapore-based SP Chemicals, will likely start test runs of its new steam cracker in Taixing, Jiangsu province, China, around August.

The steam cracker is able to produce 650,000 mt/year of ethylene.

SP Chem’s ethylene imports is likely to decline once the steam cracker is up and running.

Malaysia’s Pengerang Refining and Petrochemical, or PRefChem, is attempting to restart its new naphtha-fed steam cracker at the Pengerang Integrated Complex in the second-half of this year.

The cracker, which is able to produce 1.2 million mt/year of ethylene, is part of the RAPID project in Malaysia’s southern-most state of Johor.

Meanwhile, market participants in Asia are also keeping an eye on steam cracker operations as most of these crackers are running at full capacity despite the weak ethylene/naphtha price spread. These steam crackers are essentially supported by the relatively positive propylene-

butadiene/naphtha price spread.

“If other olefins start coming down, then steam cracker run cut may be likely. But still, spread between propylene-butadiene and naphtha is favourable for steam crackers,” a

market source said.

So far in 2019, Asian ethylene has averaged $975.65/mt CFR Northeast Asia, $1,012.23/mt CIF Northwest Europe and $323.80/mt FD USG, S&P Global Platts data showed.

US ethylene prices may head lower in H2 US ethylene spot price is the lowest among the three regions and trade sources are of the opinion that with more startups expected to come on line, US spot prices are more than likely to continue to head south.

Trade participants said that the new ethylene export terminal would likely make US ethylene prices even more competitive due to the potential demand from overseas.

However, industry sources do not expect this scenario to pan out until later in 2020.

In Asia, some market sources do not expect CFR Northeast Asia ethylene to climb above $850/mt in the near-term given the high operational run rates at existing steam crackers as well as the planned start up of new steam crackers.

Follow us on twitter @petrotahlil

END