Soaring mask demand raises Chinese polypropylene prices; China announces quality, price controls.

Petrotahlil -

Chinese fiber PP to be normalized with stricter measures

Nearly a third of Chinese PP switch to fiber grades

Surging PP lends support to upstream propylene, methanol

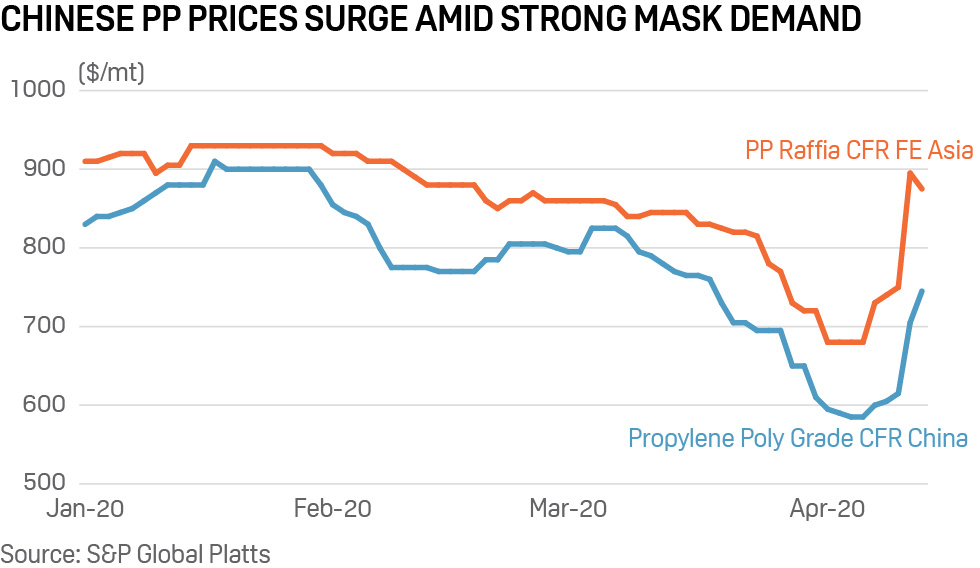

Singapore — Chinese polypropylene prices surged 35% on the week at Yuan 8,600/mt ex-works for raffia grade Monday on reduced raffia supply and stronger fiber-grade demand for making masks. The prices corrected Yuan 350/mt day on day at Yuan 8,250/mt ex-works Tuesday after the government announced strict quality and price controls amid rising demand.

Similarly, the PP CFR Fareast Asia marker was down $20/mt day on day, but up $195/mt from last Monday, at $875/mt Tuesday, S&P Global Platts data showed.

The Chinese government enforced Monday evening stricter measures to control quality and prices of medical supplies used to contain the coronavirus outbreak.

China's Jiangsu province announced subsequently to investigate and control the recent volatile prices of raw material used for masks and protective gowns like spun-bond non-woven fiber fabric, which is mainly PP fiber grade.

This pressured the China domestic PP fiber grade pellet price, which tumbled from nearly Yuan 30,000 mt/year ex-works on Monday to less than Yuan 20,000/mt ex-works Tuesday, according to sources.

However, the price remains way above other PP grades, which are generally below Yuan 10,000/mt.

Market participants said two leading Chinese state-owned companies – Sinopec and PetroChina – have taken initiatives to stabilize PP fiber prices, and plan to keep the recent popular S2040 fiber grade price below Yuan 11,500/mt ex-works, though this could not be immediately and directly confirmed with the company sources.

Chinese PP demand

Surging demand for PP fiber grade for mask and protective gowns has driven 25%-30% of Chinese PP capacities to switch to fiber grade since mid-last week, up from only 5% in March or an average of 10% in 2019, according to sources.

This has led to tighter supply for the benchmark PP raffia grade.

In addition, there are active short-covering trading activities as a major settlement for the May futures contract is round the corner, lending further support to PP raffia grades.

Nevertheless, trade participants remain concerned about overall PP demand amid the coronavirus outbreak and general bearish sentiment.

"The homo-PP production has reduced by nearly 200,000 mt in the first half of April. Spot availability is limited [for raffia grade] with trade participants holding up the cargoes, but the actual supply is enough due to the overall bearish demand from downstream," a Chinese trader said Monday.

Weak overseas demand will continue pressurizing Chinese plastics-related goods exports and demand, a source said Tuesday.

PP feedstock

Feedstock CFR China Propylene jumped $145/mt on the week at $745/mt CFR China Tuesday, as buyers tussled for both domestic and imported spot cargoes.

Demand for prompt domestic propylene was stronger than its seaborne counterpart, as fiber-grade polypropylene producers were eager to secure these materials to increase their operating rates, given the strong demand for masks.

Shandong propylene and east China prompt propylene jumped Yuan 1,400/mt and Yuan 2,500/mt on the week at Yuan 6,900/mt and Yuan 7,500/mt ex-tanks Tuesday, respectively.

But other propylene downstream markets are not convinced that demand has flipped to the bullish side.

"Only the PP producers are probably buying. We are not joining the party," said a producer that produces N-Butanol and 2-ethyl hexanol in northern China.

"The acrylonitrile market is hit mainly on demand side, the surge in propylene feedstock cost only squeezes our margins further," said an acrylonitrile producer.

The uptick in PP raffia prices provided a much-needed boost for methanol-to-olefin, or MTO, plants whose profit margins have been severely impacted by the recent fall in crude oil prices and low downstream prices stemming from an erosion of global consumer demand amid COVID-19.

The MTO to PP margin spiked to $225-$242/mt this week from $35-$90/mt last week, the highest in two years, Platts data showed.

MTO to PP margins were around $150-$190/mt in August to November last year, before tailing off as PP prices softened.

MTOs are under pressure to be viable, and the recent crash in oil prices has made MTO economics harder as it is now much cheaper for integrated petrochemical complexes to use naphtha to produce petrochemical products.

As such, this recent surge in PP prices have lifted sentiment in the methanol market, which has in the past one year been depressed by ample supply and low prices, trade sources said.

CFR China methanol prices are at 11-year lows around $169-$170/mt this week.

Follow us on twitter@petrotahlil

END